India Forecast: Strong Growth and Policy Continuity Power Investment Momentum

WHAT YOU NEED TO KNOW

- India’s political environment is expected to remain stable at the central level with low risk of abrupt policy shifts, even as a dense state election cycle shapes regional dynamics, with the Bharatiya Janata Party (BJP) strengthening coalition leverage after strong state results while Tamil Nadu and Kerala remain under regional parties.

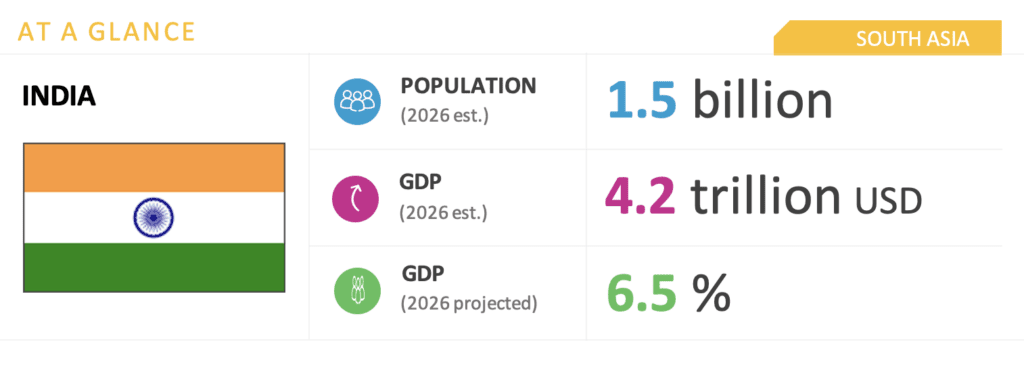

- GDP growth projections for fiscal year 2026-2027 have been revised upward to 6.5 percent by the International Monetary Fund (IMF) and 6.9 percent by the Reserve Bank of India (RBI), reinforcing India’s status as the fastest-growing major economy despite pressure from higher energy costs linked to the Iran conflict.

- The U.S.-India Bilateral Trade Agreement (BTA) is under active renegotiation following the February U.S. Supreme Court ruling overturning reciprocal tariffs, with a temporary 10 percent U.S. tariff in place for 150 days from February. 24. While India seeks to secure preferential access, the United States is using Section 301 investigation to maintain tariff pressure.

ON THE HORIZON

- The May state elections have recalibrated coalition dynamics, with the BJP’s win in West Bengal strengthening Prime Minister Narendra Modi’s federal position while expected losses in Tamil Nadu or Kerala reinforce opposition cohesion ahead of the 2029 lower house election.

- Finalizing the India-U.S. Bilateral Trade Agreement (BTA) before the 150-day tariff window expires in late July will be a key trade milestone, with a completed deal likely to boost export competitiveness in textiles, pharmaceuticals, electronics and technology services.

- India’s response to the Iran conflict will deepen in the second half, with expanded ethanol blending mandates across aviation and maritime sectors and continued prioritization of strategic petroleum reserve replenishment.

- India Semiconductor Mission (ISM) 2.0, with an enhanced outlay of INR 4 trillion, ($42.4 billion) is expected to advance approved projects and attract additional global semiconductor investment.

- India is moving toward tighter artificial intelligence (AI) governance, with new rules expected on synthetically generated content, continuous labeling and traceability and takedown compliance.

India Market Overview and Forecast

Political Climate

Post-Election Recalibration Shapes Modi’s Federal Agenda

The second half of 2026 will be shaped by the May assembly results in Assam, Kerala, Tamil Nadu, West Bengal and Puducherry. These are relevant for multinational corporations because Indian states control land, power, labor administration, sector incentives and operating permissions. The base case is policy continuity at the center under the BJP-led National Democratic Alliance, with infrastructure capital expenditure and manufacturing execution largely intact. The main risk is state-level execution volatility as new governments fund welfare priorities and reset compliance and inspection intensity.

The BJP’s historic win in West Bengal was a key national swing — the first decisive breakthrough in a state long dominated by the left and then the ruling Trinamool Congress Party. The victory signals sharper organization and wider public approval, strengthening Modi’s political image, coalition leverage and in turn supporting faster project execution in logistics and eastern supply chains.

Investors should actively engage Tamil Nadu’s new government to verify continuity of Dravida Munnetra Kazhagam-era commitments on electronics, autos, data centers and global capability centers (GCCs) — given the current dispensation’s lack of any prior governance track record; Kerala’s ports, logistics and labor relations; and Assam’s and Puducherry’s corridor and ease-of-doing-business signaling. Key factors on businesses’ watch lists should be state budget rollouts, large-project clearances, law-and-order hotspots and any incentive-policy revisions.

Geopolitically, India’s strategic autonomy doctrine continues to navigate competing pressures. The Iran conflict has forced a pragmatic energy security calculus: India resumed Iranian crude imports in the first quarter of 2026 for the first time since 2019, generating friction with Washington even as the U.S.-India BTA negotiations advance. India will seek to manage this tension through diplomatic channels while maintaining its nonaligned energy posture.

Macroeconomic Climate

Resilient Domestic Growth, but Energy Costs and Trade Uncertainty Cloud the Horizon

India’s growth trajectory remains the strongest among major economies, though the country faces headwinds from the Middle East conflict and elevated fuel prices. The IMF projects GDP growth of 6.5 percent for fiscal year 2026-2027, while the RBI forecasts a more optimistic 6.9 percent driven by domestic consumption, range-bound inflation, income tax reforms and front-loaded government capital expenditure. Two landmark trade deals — with the European Union and New Zealand — and an India–U.S. interim trade deal in its final stretch with U.S. Chief Negotiator Brendan Lynch in New Delhi from June 1-4 to finalize details create a meaningful medium-term offset by broadening India’s export base and external account resilience. Three macroeconomic scenarios are possible amid the global energy crisis:

Upside Scenario: Deescalation of the conflict brings crude prices down, easing fiscal and inflationary pressures. The rupee stabilizes as foreign portfolio flows reverse, supported by robust reserves. The trade deals gain traction, boosting labor-intensive manufacturing exports and services through eased regulatory barriers. GDP growth trends toward the RBI’s 6.9 percent forecast, with inflation settling in the lower half of the tolerance band. The government meets its 4.3 percent fiscal deficit target.

Moderate Scenario: India sustains 6.5 percent GDP growth (IMF baseline), but elevated crude forces difficult fiscal trade-offs — excise cuts, subsidies, credit support and oil marketing companies’ absorption limit pass-through. Inflation averages 4.6 percent, with periodic food and fuel-driven spikes. The rupee faces continued but managed depreciation, with the RBI smoothing volatility through spot and forward interventions. Trade deals progress but benefits materialize gradually. Even under energy shock scenarios, the IMF projects 6.1-6.2 percent growth — more than twice the global average.

Downside Scenario: A prolonged conflict sustains crude above shock thresholds, eventually forcing fuel price pass-through that accelerates inflation and weakens consumer spending. The rupee depreciates further, raising input costs and compressing margins. Foreign portfolio outflows intensify amid global risk aversion. The fiscal deficit overshoots 4.3 percent as subsidy bills mount. GDP growth moderates toward 6.1-6.2 percent, with risks to even this floor if trade disruptions, secondary sanctions or delays in deal implementation compound energy pressures.

Investment Environment

Supply Chain Realignment, Semiconductor Scale-Up and Energy Transition Drive Investment

Investment momentum is expected to focus on supply chain relocation to India, execution of India Semiconductor Mission 2.0 and energy security-driven clean energy build-out. Multinational corporations should align capital expenditure, supplier onboarding and market entry plans with evolving trade rules, standards and state incentives.

Trade and market access: A U.S.-India trade arrangement in the second half would accelerate foreign direct investment in electronics, pharmaceuticals, textiles and aerospace and prompt adjustments to sourcing rules and tariffs. Parallel agreements with the United Kingdom and Gulf Cooperation Council would strengthen India’s role as an export platform.

Electronics and supply chains: Production-linked incentive expansion by original equipment manufacturers will continue, with localization opportunities in components, electronics manufacturing services, testing and repair and logistics for firms meeting quality and scale requirements.

Semiconductors: ISM 2.0 has launched with a $960 million program focused on equipment, materials and intellectual property to address the upstream gaps left by ISM 1.0. The coming months will likely see a focus on execution quality and supplier development timelines.

Energy transition: Energy security concerns will support investment in solar manufacturing, transmission, battery energy storage systems and green hydrogen. Sustainable aviation fuel policy progress could unlock demand, with blending mandates and offtake clarity as key triggers.

Digital infrastructure and GCCs: Data center and AI build-out will continue, supported by state-level incentives. Implementation of the Digital Personal Data Protection Act should improve compliance certainty for IT services and GCCs.

We will continue to keep you updated on developments in India as they occur. If you have any questions or comments, please contact BGA India Managing Director Anuj Gupta at agupta@bowergroupasia.com.

Best regards,

BGA India Team