Japan Forecast: Strategic Investment Push Meets Rising External Risks

WHAT YOU NEED TO KNOW

- Prime Minister Sanae Takaichi is expected to enter the second half of 2026 with exceptionally strong political momentum, providing a favorable environment for medium- to long-term policy execution.

- Japan’s economy will likely remain relatively resilient. GDP growth is forecast around 1 percent, supported by wage growth, exports and inbound demand, though weak real income and elevated energy prices continue to weigh on consumption.

- The administration’s push across 17 strategic sectors — including artificial intelligence (AI), semiconductors, the green transformation, hydrogen, defense and advanced manufacturing — is creating new opportunities for foreign investors through subsidies, tax incentives and infrastructure support.

- Energy security, particularly risks tied to the Middle East crisis and oil procurement, remains the largest threat to political stability, consumer sentiment and broader economic performance.

ON THE HORIZON

- Mid-year 2026 Cabinet reshuffles and party leadership appointments will serve as a key test of Takaichi’s ability to consolidate internal political power. Upcoming green transition strategic zone designations this summer, particularly in regions such as Kyushu and Hokkaido, may unlock substantial investment opportunities in data centers, energy infrastructure and industrial clusters.

- The Bank of Japan is expected to raise interest rates at the June Monetary Policy Meeting but will remain cautious. Still, yen weakness, inflation pressures and external shocks could reshape monetary policy and investment conditions.

- Stabilization in global energy markets could improve growth prospects, while prolonged geopolitical disruption could significantly raise recession or stagflation risks.

Japan Market Overview and Forecast

Political Climate

Takaichi Administration: Strong Start, Energy Risks and Test of Political Consolidation

The Cabinet led by Sanae Takaichi will likely begin the second half of 2026 with exceptionally strong public approval ratings, approaching 70 percent. While conservative priorities such as constitutional revision are not widely regarded as immediate policy imperatives, they appear to enjoy a meaningful degree of public support. Likewise, efforts to strengthen defense capabilities and promote arms exports have not generated major political backlash. These policy directions are broadly a continuation of trends that advanced during the rule of former Prime Minister Shinzo Abe.

Nevertheless, there is no guarantee such high approval ratings will endure. The most significant risk is a prolonged disruption in the Strait of Hormuz, resulting in higher energy prices and wider economic spillover. Japan has historically imported more than 90 percent of its crude oil through the strait. Even with strategic stockpiles exceeding 200 days, alternative sourcing and rerouted shipping would likely involve substantial additional costs. Normalization could take considerable time, even after the immediate crisis subsides. Takaichi is expected to pursue a pragmatic energy policy package that includes nuclear power, renewable energy expansion and the diversification of procurement sources.

At the same time, concerns are beginning to emerge within the ruling Liberal Democratic Party over a management style perceived as overly centralized and inclined toward personal decision-making. The Cabinet reshuffle and party executive appointments expected this summer will be an important test of how effectively Takaichi can strengthen her internal political base.

On foreign policy, the U.S.-Japan relationship — particularly Takaichi’s strong personal rapport with President Donald Trump — represents a major political asset for the Japanese administration. No national elections are scheduled until the summer of 2028, giving the prime minister a politically favorable period of stability.

Macroeconomic Climate

Resilient Growth Under Energy and Geopolitical Uncertainty

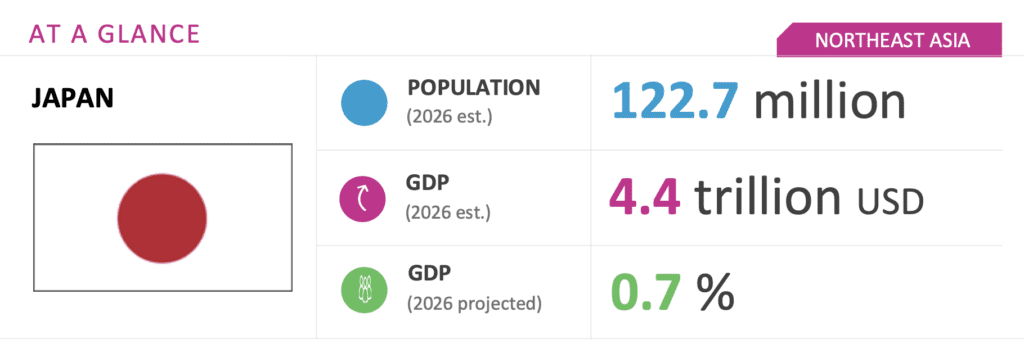

Although the Japanese economy has entered a deceleration phase since 2025, it is expected to remain relatively resilient through the second half of 2026, supported by continued momentum in wage increases. While exports and inbound tourism demand are maintaining a steady pace, rising geopolitical tensions in the Middle East have pushed gasoline prices up by about 20 percent since February. In addition, higher import prices are driving up inter-firm transaction costs. As a result, private consumption remains weak, constrained by sluggish growth in real income.

Real GDP growth is expected to remain around 1 percent this year. Looking ahead, the outlook is highly dependent on energy prices and external demand conditions. The government passed a supplementary budget for fiscal year 2026 June 5 totaling JPY 3 trillion ($18.7 billion) to fund measures such as gasoline subsidies. However, some government officials have begun to express concern that difficulties in procuring energy resources, including crude oil, could further slow global economic activity — particularly in Southeast Asia — and increase the risk of a synchronized global downturn, making Japan’s outlook variable.

Upside Scenario: Early stabilization of the Middle East situation would lead to lower energy prices and improved terms of trade for Japan. Reduced inflationary pressure would support a recovery in real incomes and private consumption. Combined with a weaker yen, exports and inbound tourism could expand further, pushing growth up to around 1.5 percent.

Moderate Scenario: Prospects for crude oil procurement are expected to be secured within the year, preventing severe disruptions to energy supply. Crude oil prices remain elevated, and while external demand stays firm, real wage growth is modest, resulting in a slow recovery in consumption. The Bank of Japan will likely maintain a wait-and-see stance, with growth hovering around 1 percent.

Downside Scenario: A prolonged conflict disrupts energy supplies, and rising import costs reignite inflation, further eroding real incomes and depressing consumption. A global recession or stagflation could emerge, weakening external demand and putting downward pressure on corporate earnings and investment. Economic growth could approach zero or even turn negative.

Investment Environment

Government-Led Investment Push in Strategic Industries Amid External Risks

Takaichi has positioned investment in 17 strategic sectors as a core policy pillar from the perspective of economic security and technological innovation. Efforts are underway to prioritize these sectors, creating significant opportunities for foreign investors. Targeted areas include AI and semiconductors, quantum technology, biotechnology, aerospace, green transition, cybersecurity, shipbuilding and defense. The government is expected to deploy “investment-inducement policies” combining subsidies, tax incentives, government guarantees and infrastructure development, making market entry pathways clearer. For each sector, the government is developing road maps identifying key technologies and products, increasing clarity around investment targets.

In the AI, semiconductor and data infrastructure sectors, initiatives will integrate advanced semiconductor manufacturing with data centers and the expansion of power and telecommunications infrastructure. This summer, the government is expected to announce designated candidate regions for Green Transformation Strategic Zones — likely including Kyushu and Hokkaido — where consortium formation and joint ventures centered on data center clusters are expected to accelerate.

In the energy sector, long-term public-private investment will expand in areas such as hydrogen, ammonia, renewable energy and next-generation power grids. These developments may support overseas infrastructure investors and energy companies seeking to expand through project finance, technology provision and operational participation. In sectors such as biotechnology, pharmaceuticals, quantum technology, aerospace and defense, the government is actively encouraging investment through research and development tax incentives and large-scale fiscal support.

We will continue to keep you updated on developments in Japan as they occur. If you have any comments or questions, please contact BGA Japan Managing Director Kiyoaki Aburaki at kaburaki@bowergroupasia.com.

Best regards,

BGA Japan Team