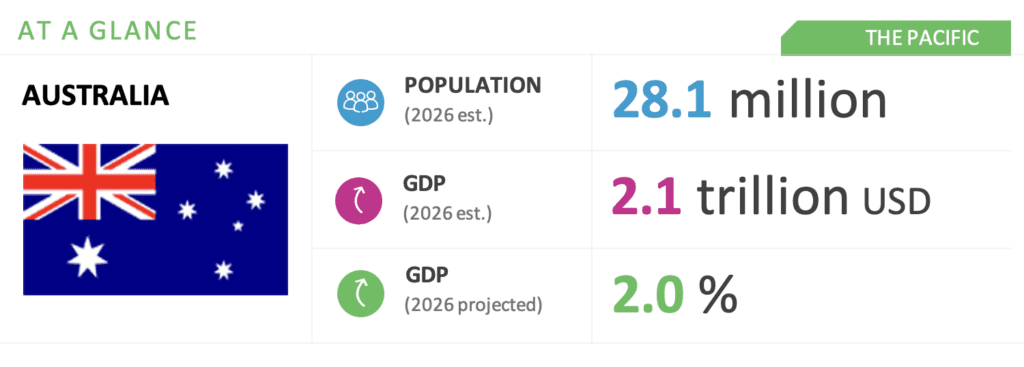

Australia Forecast: Mounting Political Pressure and Energy Tensions Amid a Slowing Economy

WHAT YOU NEED TO KNOW

- The Labor government has entered its most challenging period after its 2025 landslide victory. Although it is expected to win the next election, a poorly received May 12 budget has cost it support. While support for major parties has declined since the last election, traditional conservatives have lost the most.

- Unemployment is low, and consumer spending is resilient. However, real wages are falling amid weak productivity and persistent inflation, while higher interest rates and petrol prices have reduced confidence.

- Social cohesion is generally strong, though the December 2025 Bondi Beach terrorist attack has elevated immigration as a key political issue alongside economic concerns.

- Australia is deepening its security partnership with the United States while strengthening trade ties in Asia and beyond.

- The Iran conflict has sparked debate over energy security and the feasibility of ambitious renewable energy targets. The government is highlighting “sovereign renewables.”

ON THE HORIZON

- The government will continue engaging key fuel suppliers across Asia, highlighting Australia’s role as a supplier of liquefied natural gas (LNG).

- Unemployment is expected to rise, and inflation will likely remain above the Reserve Bank’s target range.

- Higher prices for key exports, such as LNG, may offset growing budget pressures, though calls to cut government spending will persist.

- The government will seek investment in artificial intelligence (AI), data centers, renewable energy and critical minerals. Corporate Australia will push for changes to foreign investment approvals and corporate taxation.

- The government will pursue an east coast gas reserve amid slowing renewable investment, calls to raise taxes on LNG exporters and rising industry concerns over environmental laws.

- The November election in Victoria — its long-standing Labor government is widely seen as Australia’s most left-wing — will be closely watched for federal implications.

- Prime Minister Anthony Albanese may reshuffle his Cabinet by the end of 2026, around the midpoint of the parliamentary term.

Australia Market Overview and Forecast

Political Climate

Urban Australia Remains the Government’s Stronghold

While surveys show support for major parties has fallen since the last election, the Labor government appears on track for victory in the next election, due by 2028. Australia’s ranked and compulsory voting system means elections are won in the political center. The Labor Party has adjusted better than the Liberal-National opposition in building a winning strategy to capture middle Australia, particularly in the cities among multicultural communities, women and younger Australians. The rise of the right-wing populist One Nation Party — sympathetic to the administration of U.S. President Donald Trump — has largely come at the expense of the Liberal-National coalition, although a lesser shift has recently occurred among traditional Labor voters.

A key theme of the 2026-2027 budget was addressing intergenerational equity by reducing tax concessions for housing investors to favor first-time homebuyers. However, this has been poorly received because much of middle Australia’s perceived wealth is linked to rising housing prices, and Prime Minister Albanese repeatedly ruled out such changes before the 2025 election. Furthermore, proposed capital gains tax changes targeting other asset classes have been criticized for allegedly undermining aspiration and entrepreneurialism.

Macroeconomic Climate

Slowing Economy

Inflation picked up significantly in the second half of 2025, compounded by the Iran war. The Reserve Bank of Australia forecasts inflation to peak at 4.8 percent in June and fall to 4 percent in December, unemployment to remain around 4.3 percent for the rest of the year and the cash rate to increase to 4.7 percent by the end of 2026. Household credit growth has been weak over the past six months, with consumer sentiment falling due to rising petrol prices and interest rate rises. Government spending has increased as a share of GDP, with budget deficits and government debt projected to grow in the next decade. The government is reducing growth in spending, notably on the National Disability Insurance Scheme.

The cost of the energy transition, largely underwritten by taxpayers, is in the spotlight. Immigration continues to stimulate demand, but it has put pressure on housing affordability, infrastructure and services. The slowing economy and May 12 budget have contributed to a dip in housing market activity. The global economic downturn creates several variables for Australia’s economy in the coming months:

Upside Case: Military operations in Iran end quickly, followed by the normalization of energy production and shipments and oil prices returning toward pre‑conflict levels. This results in limited global market disruption, and Asia and Europe recover without significant GDP damage. GDP growth picks up with strong growth in consumption, and business and dwelling investment resume. The outlook for business investment and exports strengthens, supported by spending related to technology and the energy transition and resilient trading partner growth (underpinned by the global AI boom).

Moderate Case: Military operations continue for several weeks before winding down. Oil prices remain elevated, but global supply is not severely disrupted. Risk aversion stays higher for longer; growth slows for several months. Oil prices remaining around US$100 per barrel lifts headline inflation in Australia to about 5 percent over the next year to the June quarter, around 0.75 percentage points higher than had been expected in February. Costs for firms rise, and some of this is passed on to consumers. Higher energy prices constrain the economy’s productive capacity, depressing output. However, while Australia is a net importer of oil, it is a net exporter of energy. Higher LNG prices lift export revenue and raise national income.

Downside Case: Prolonged conflict disrupts global energy supplies, driving oil prices sharply higher and negatively impacting growth and inflation. Europe and Asia face recession risks, financial conditions tighten, credit risk rises and central bank policy becomes more constrained. Prolonged higher oil prices lead to higher inflation, rising interest rates, recession and an unemployment rate above 6 percent in 2026. Oil-supplying countries stockpile, reducing availability to Australia. However, banks are in a strong position to continue supporting the economy in a severe economic downturn.

Investment Environment

Government Courting Technology Investment

Imports are forecast to continue to grow solidly at 3.5 percent in 2026-2027 and 3 percent in 2027-2028. The Reserve Bank notes investment growth is expected to continue in sectors “with strong structural tailwinds” such as software, data centers and renewable energy. The 2026-2027 budget’s productivity package aims to cut compliance costs and unlock research and development investment by young firms. The government will abolish an additional 497 “nuisance tariffs” starting July 1.

The Treasury Department now assesses that it will take an additional five years, rather than two years, to lift Australia’s relatively low productivity growth to around the long-term average of 1.2 percent. The corporate sector wants a more internationally competitive corporate tax rate, streamlined foreign investment approvals, flexible labor laws, reduced government spending, a higher education system geared more toward economic needs and a more orderly energy transition. Canberra views AI as a lever to address sluggish productivity and wants Australia to become a global data center hub. The government expects data center operators to support Australia’s energy transition, train and employ Australians and support domestic startups.

The government’s proposed domestic gas reservation scheme will see east coast gas exporters forced to set aside 20 percent of future gas production for domestic supply. Australia and the United States have committed more than AUD 5 billion (US$3.5 billion) to back a range of critical mineral projects, nearly double the amount pledged when Trump and Albanese struck an agreement in October. Australia seeks to diversify its markets. It has concluded free trade negotiations with the European Union and is working toward a free trade agreement with India. Albanese and colleagues have visited key fuel-supplying countries across the region — including Singapore, Japan, Korea, China, Malaysia and Brunei — and noted that Australia remains a vital supplier of LNG across Asia.

As part of the National Defense Strategy, the government is investing in autonomous capabilities, accelerating the introduction of air and missile defense capabilities, acquiring Mogami-class frigates from Japan, delivering Australia’s Guided Weapons and Explosive Ordnance enterprise and progressing the Australia-United Kingdom-United States (AUKUS) submarine program.

We will continue to keep you updated on developments in Australia as they occur. If you have any questions or comments, please contact BGA Australia Managing Director Michael “Mick” McNeill at mmcneill@bowergroupasia.com.

Best regards,

BGA Australia Team