China Forecast: Resilient Growth Amid Weak Demand and Targeted Investment Opportunities

WHAT YOU NEED TO KNOW

- China’s economy remains resilient, but the recovery is uneven. Weak domestic demand is the most persistent risk, and current policy settings leave room to respond if conditions deteriorate.

- China recorded GDP growth of 5 percent in the first quarter, beating expectations on strong exports and high-tech manufacturing. Domestic demand has stayed weak. Retail sales slowed to just 0.2 percent in April, the lowest in more than three years, while exports kept climbing. Household income accounts for around 43 percent of national income in China, versus a global average closer to 60 percent.

- The 15th Five-Year Plan (2026-2030), approved in March, makes technological self-reliance and industrial upgrading China’s top priorities, with artificial intelligence (AI), semiconductors, advanced manufacturing and green technology at the center. It also signals a rebalancing of fiscal spending toward households and social welfare.

ON THE HORIZON

- Xi Jinping and U.S. President Donald Trump met in Beijing in mid-May. The two sides agreed to set up a “board of trade” and a “board of investment,” a framework for cutting tariffs and Chinese purchases of at least $17 billion in U.S. farm goods a year plus an initial order of 200 Boeing jets. The summit steadied the relationship but left the bigger disputes unresolved. The leaders plan to meet again in the fall.

- Xi’s current term ends in 2028. If he does not seek a fourth term, successor positioning within the party apparatus may become visible over the next year.

- Third and fourth quarter GDP results will be the first clear indication of which of the three macroeconomic scenarios is materializing.

- Sub-plans under the Five-Year Plan, including the urban-rural income growth plan and the hukou household registration reform implementation details, are expected in the latter half of the year.

- In May, regulators issued their first ruling under companion Decree 835, against the European Union’s investigation of Chinese firm Nuctech. The first cases under Order No. 834 (Article 15) have yet to come.

China Market Overview and Forecast

Political Climate

Core Policy Agenda Remains Unchanged

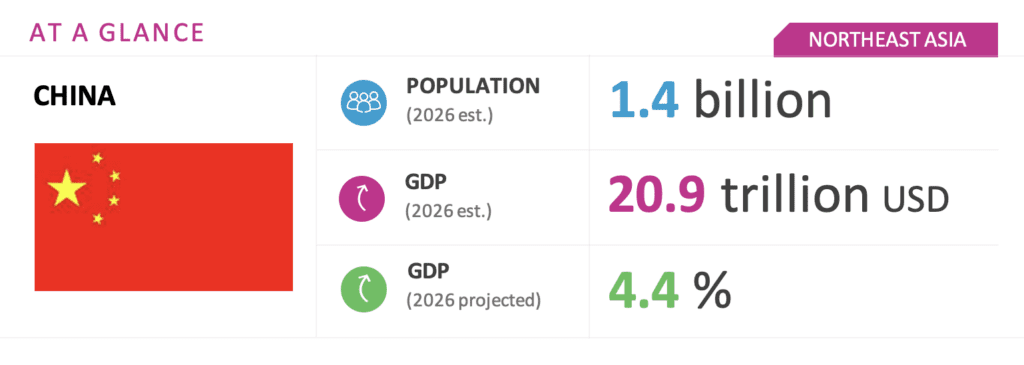

The “two sessions” concluded in March, with the National People’s Congress approving the 15th Five-Year Plan (2026-2030). The plan sets the policy framework for the next five years and reaffirms a fiscal deficit-to-GDP ratio of around 4 percent, leaving scope for easing if conditions deteriorate in the second half of 2026. Public budget expenditure will exceed CNY 30 trillion ($4.4 trillion) for the first time.

Fiscal tools include CNY 1.3 trillion ($191 billion) in ultra-long special treasury bonds (250 billion for consumer trade-in programs, 300 billion for state-owned bank capital) plus CNY 4.4 trillion ($647 billion) in local government special-purpose bonds. The defense budget rose 7 percent. The April 28 Politburo readout confirmed “major indicators have beaten expectations,” reiterated precision in monetary policy and renminbi stability. It also flagged the “AI plus” action plan, six infrastructure networks (water, electricity grid, computing power, next-generation communications, urban underground pipeline and logistics) and urban renewal and new urbanization as key tools for stabilizing the property market. China’s foreign policy continues to oppose protectionism while remaining committed to multilateral engagement and trade diversification. Under the pressure of U.S. tariffs, several members of the Organization for Economic Cooperation and Development have moved to deepen economic ties with China, softening the “small yard, high fence” dynamic of 2021-2024. Whether Xi serves a fourth term beyond 2028 is unclear; either way, party solidarity and centralization will remain leading principles.

Macroeconomic Climate

Growth Holds as External Shocks and Domestic Demand Drive Downside Risks

First-quarter GDP rose 5 percent year on year, helped by a 14.7 percent jump in exports and strong high-tech manufacturing. Retail sales lagged at 2.4 percent, then fell to 0.2 percent by April. The Iran war has pushed inflation back above 1 percent, with the April consumer price index at 1.2 percent, and the People’s Bank of China has held the loan prime rate at record lows for 12 straight months. Exports stayed strong, up 19.4 percent in May as firms rushed orders. What matters most for the second half of 2026 is how the Iran war develops and how it feeds through to oil prices, shipping and partner-country demand. So far, the moderate scenario looks closest to events. Oil has dropped about 20 percent from its 2026 peak to around $90 a barrel, and shipping through the Strait of Hormuz is slowly resuming under a shaky ceasefire.

Upside Scenario: A quick end to military operations in Iran and the reopening of the Strait of Hormuz pull oil back toward pre-conflict levels by early in the third quarter. Export volumes recover and full-year growth lands at the top of the official 4.5-5 percent band. The People’s Bank of China (PBOC) holds policy steady and fiscal disbursement proceeds at the announced pace, with no supplementary package required. Tier-1 property stabilization continues, and the new urban-rural income growth plan begins to register in services consumption late in the year.

Moderate Scenario: Military operations continue for several weeks before winding down. Oil stays elevated, but global supply is not severely disrupted. Shipping costs and external demand remain softer than in the first half of the year, pulling third-quarter export growth below historical trends and producing only a partial recovery in the fourth quarter. Full-year growth settles near 4.5 percent, in line with the IMF. Beijing accelerates the announced fiscal pipeline: the CNY 1.3 trillion ($191 billion in ultra-long special treasury bonds and the CNY 4.4 trillion ($647 billion) in local government special-purpose bonds are disbursed faster than originally planned. The loan prime rate stays at record lows, and the PBOC continues to defend renminbi stability.

Downside Scenario: Prolonged conflict cuts into global energy supply. Oil prices rise sharply, lifting global inflation and damaging external demand. China’s 1 billion barrels of strategic reserves and its diversified energy mix limit the price hit at home, but sustained shipping disruption and weaker partner demand cut exports materially. Full-year growth falls below 4 percent. Global financial conditions tighten, raising credit risk and narrowing the PBOC’s room to ease. Beijing breaks the 3 percent fiscal-deficit norm, issues a supplementary special-bond tranche and brings forward hukou reform and income-support measures to defend consumption. The property drag deepens as local government balance sheets come under further strain.

Investment Environment

Sectoral Opportunities and Risks

Priority sectors for policy support and capital access in the second half of the year include integrated circuits, aerospace, biomedicine and the emerging sector economy. The plan also identifies long-cycle bets in embodied AI, quantum technologies, 6G and brain-computer interfaces. Daily AI token usage exceeded 140 trillion as of March, up 40 percent from the end of 2024, signaling concrete demand for compute and applications across both foreign and domestic suppliers. Services opening-up continues: pilots for wholly foreign-owned hospitals, value-added telecoms and biotechnology are now operational, with education and culture being opened in an “orderly manner.” This is a credible entry window for service-sector investors in the latter half of the year.

On the risk side, foreign investment in advanced semiconductors, critical infrastructure and national security faces heightened scrutiny. State Council Order No. 834 (7 April 2026) establishes China’s first dedicated industrial and supply chain security regulation. Article 15 authorizes investigations and countermeasures against foreign entities whose conduct causes substantial harm. A companion rule, Decree 835, was used for the first time in May, against the European Union’s investigation of Nuctech. Foreign manufacturers should assess their exposure before making commitments in the second half of the year. Property remains the most significant structural drag: fixed-asset investment in the sector fell 17.2 percent in 2025, no broad-based bailout has been signaled and local government balance sheets are stressed by land revenue declines. Tier-1 cities are progressing on stabilization, but tier-2 and tier-3 markets remain under pressure and will weigh on investment through 2026.

We will continue to keep you updated on developments in China as they occur. If you have any comments or questions, please contact BGA Adviser Eric Wang at ewang@bowergroupasia.com or Director Sam Overholt at soverholt@bowergroupasia.com.

Best regards,

BGA China Team