Energy Transition Navigates Challenging Geopolitics: Energy, Climate and Resources Forecast

WHAT YOU NEED TO KNOW

- Indo-Pacific markets are adjusting their energy strategies in response to U.S. trade policy changes and fossil fuel production growth. Countries are increasing U.S. liquefied natural gas (LNG), biofuel and crude oil imports while diversifying sources from Russia, the Middle East and Southeast Asia.

- Technological adoption is speeding up renewable energy deployment despite challenges from U.S. policies and geopolitical uncertainty. Nevertheless, power demand still outpaces renewables. Low-carbon tech like solar, wind and batteries is still gaining momentum in the region, while prospects for carbon capture and hydrogen remain more uncertain.

- Talks with Indo-Pacific partners on the Alaska LNG pipeline have resumed, with interest from more than 50 countries and markets totaling more than $115 billion in potential contract value. Japan, Korea and Taiwan remain key players. The project will impact LNG prices by increasing supply, boosting competition and lowering costs for consumers. A final investment decision on the pipeline’s domestic portion is expected by year’s end.

- The U.S. reliance on critical minerals underscores the need for a resilient supply chain, especially given China’s dominance. Indonesia, a major nickel producer, plays a crucial role. Washington is boosting domestic output and strengthening ties with Australia and Canada, but recent tariffs on Southeast Asian solar panels may strain partnerships.

ON THE HORIZON

- The cost of the global transition to green technology is expected to increase as U.S. energy policies are implemented. China may adjust its low-carbon exports amid tightening trade barriers, resulting in increased local manufacturing. Meanwhile, Southeast Asian nations are expanding cross-border energy cooperation to share resources and technology.

- Indo-Pacific governments are expected to adopt protective measures to promote energy independence. India and Indonesia may revise tariffs on imports to support domestic output, while Vietnam and the Philippines pursue infrastructure investments and energy diversification.

- The region is preparing for advances in renewable energy, with increased public and private investments in hydrogen production supported by subsidies in Japan, Korea and Europe.

- Fossil fuel power generation will likely increase in the Indo-Pacific despite the recent growth in renewables. Markets are balancing immediate energy needs with investments in clean energy technologies, storage and transmission for a more sustainable future.

Sector Overview and Forecast

Macrotrend Monitor

The Indo-Pacific is witnessing a robust push toward clean energy technologies, with substantial investment in renewables, hydrogen and carbon capture strategies. Countries such as Thailand and Vietnam are introducing incentives like Thailand’s first green electricity tariff and Vietnam’s decree on renewable energy. Others like Indonesia and Malaysia are enacting progressive laws to expand the scope of carbon capture and storage, reflecting a growing dedication to emissions reduction. These initiatives underscore a regional commitment to fostering sustainable energy systems backed by government support and regulatory frameworks.

AI and Electricity Demand

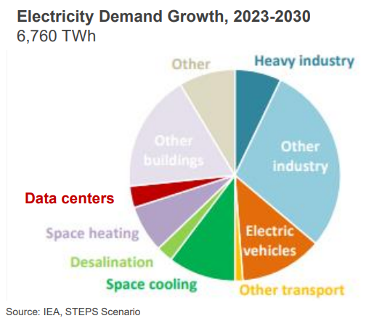

Artificial intelligence (AI) presents a paradigm shift in how energy is generated, distributed and consumed. China is leading in AI model training, leveraging its affordable renewable energy and abundant data. Around the region, as international oil companies and national oil companies position themselves in the AI sector, they aim to optimize energy supply while exploring AI applications across the energy value chain. The intersection of AI, energy and national security also introduces geopolitical complexities, with countries prioritizing energy independence as they develop AI technologies. Although data centers may heighten local grid demand, economic expansion, industry electrification and electric vehicle adoption will significantly impact energy use across the region. The discourse on decarbonization targets will continue to evolve as energy majors argue for extended fossil fuel reliance, citing an anticipated spike in power demand to support AI.

Energy Transition

The energy transition landscape in the Indo-Pacific is marked by competing ambitions, which are reflected in nationally determined contributions and geopolitical aspirations. Upcoming negotiations at the 2025 United Nations Climate Change Conference (COP30) follow a challenging COP29. Critical discussions on climate finance and fossil fuel policies are expected when leaders meet in Brazil in November. The results of these negotiations will likely influence the level of ambition in nationally determined contributions, particularly as the European Union reasserts its climate leadership amid the complexities posed by emerging alliances such as BRICS.

Despite an upward global trend in renewable energy, coal-fired generation is projected to hit record levels in 2025, with China leading the charge as it continues to expand its coal fleet. India and Southeast Asia are similarly reliant on coal to meet burgeoning electricity demands. In contrast, nuclear power is reemerging as a viable alternative, with output expected to reach new highs in 2025, highlighting a multifaceted approach to energy generation within the region.

Subsector Highlight

Critical Minerals Under US Scrutiny and Clean Energy Impact

The critical minerals market is currently under intense scrutiny from U.S. officials seeking to address market distortions linked to U.S. dependence on key minerals such as lithium, nickel and cobalt. China currently dominates the critical minerals supply chain, processing significant volumes of essential minerals and manufacturing components for clean energy technologies. Indonesia continues to play a significant role in lithium, cobalt and nickel production, controlling more than half of global nickel processing as a key player for companies operating in the Indo-Pacific.

The U.S. Department of Commerce launched an investigation to address U.S. critical minerals dependencies under Section 232 of the Trade Expansion Act. Washington will likely focus on boosting domestic mineral production while fostering relationships with allied countries such as Australia and Canada to create a more resilient supply network.

In a significant escalation, President Donald Trump has moved to invoke emergency powers under the Defense Production Act to fast-track domestic critical mineral projects. This includes waiving funding thresholds and approval timelines and enabling the faster deployment of resources to counter foreign supply chain dominance. The administration views this as a necessary step to secure long-term U.S. industrial and military resilience amid growing geopolitical tensions.

Recent U.S. measures also include tariffs on solar panels imported from Indo-Pacific countries, including Cambodia, Malaysia, Thailand and Vietnam, as part of its broader trade strategy to protect its burgeoning clean energy industry. While the tariffs aim to reinforce domestic production capabilities, they also complicate relationships with Southeast Asian economies that are integral to the global supply chain. This marks a pivotal moment for clean energy dynamics regionally and globally.

Looking ahead, the United States will need to strategically navigate its partnerships to avoid infringing on the sovereignty of resource-rich nations and provoking economic retaliation from China. For its part, China will likely continue leveraging its established relationships through economic assistance and subsidies, employing comprehensive strategies to maintain its stronghold in the critical minerals domain. This rivalry complicates the environment for resource-rich countries in the Indo-Pacific, which may struggle to balance competing foreign influences on their mineral sectors.

We will continue to keep you updated on developments in the energy, climate and resources (ECR) sector as they occur. If you have comments or questions, please contact BGA Director Chayamon “Amm” Srisongkram at csrisongkram@bowergroupasia.com.

Best regards,

BGA ECR Team