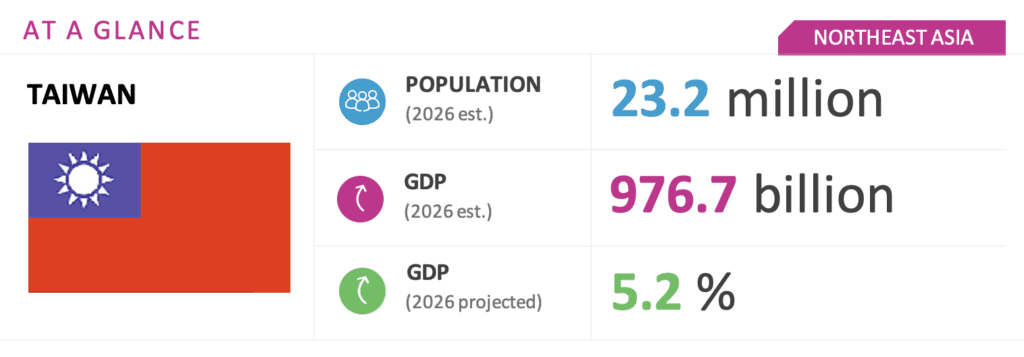

Taiwan Forecast: Strong AI Growth Amid Political Headwinds and Energy Pressure

WHAT YOU NEED TO KNOW

- Taiwan secured two bilateral agreements with the United States: a January semiconductor memorandum of understanding (MOU) granting preferential tariffs and committing US$500 billion in investment, and a February Agreement on Reciprocal Trade (ART) setting a 15 percent non-stacking tariff rate while reducing Taiwan’s tariffs on U.S. goods. The ART is now being renegotiated after a U.S. Supreme Court decision prompted the administration of Donald Trump to seek a new legal basis for the deal.

- President Lai Ching-te announced a review of restarting decommissioned nuclear plants, signaling a shift from the Democratic Progressive Party’s (DPP) long-standing “nuclear-free homeland” stance.

- Taiwan is advancing the Ten AI Initiatives Promotion Plan as a top industrial priority, directing public investment toward silicon photonics, quantum computing, artificial intelligence (AI) robotics and computing infrastructure.

ON THE HORIZON

- Taiwan’s quadrennial local elections, covering offices from mayors and city councilors to neighborhood chiefs, will take place Nov. 28 and serve as a midterm test for President Lai, with a weak DPP showing potentially undermining his standing within the party and shaping the 2028 presidential race.

- The government will prioritize pocketbook issues affecting livelihoods and local economies, particularly small and medium enterprises, while seeking to stabilize utility prices despite rising global oil and gas costs.

- Taiwan aims to finalize revisions to the ART with the United States after Section 301 investigations around July, seeking to preserve gains from earlier agreements, though opposition parties may use legislative review to delay or block progress.

- Ongoing Middle East conflicts may keep oil and gas prices elevated, increasing financial pressure on state-run CPC and Taipower and reinforcing the case for energy diversification.

Taiwan Market Overview and Forecast

Political Climate

Taiwan’s Election-Year Politics to Heighten Policy and Cross-Strait Sensitivities

Taiwan will hold local elections November 28, about one year before the presidential and legislative elections expected in January 2028, making them the final major test before the national vote. While campaigns will center on local issues such as transportation, housing, child care and infrastructure, results will influence party morale, opposition coordination and perceptions of President Lai’s reelection prospects. A major defeat for the DPP would weaken President Lai’s leadership and 2028 momentum, while gains in key races would help stabilize the administration.

A key issue is whether the Kuomintang (KMT) and Taiwan People’s Party (TPP) can convert legislative cooperation into a durable electoral alliance. Early coordination through joint nominations is underway. If sustained, it would increase the likelihood of a consolidated opposition bloc in 2028, complicating Lai’s reelection and encouraging a harder legislative approach.

Cross-strait tensions will remain elevated, but the risk of direct military conflict is low. Beijing will favor gray-zone activity, economic and diplomatic pressure and selective engagement with opposition figures, aiming to weaken the Lai administration and test KMT-TPP cooperation ahead of 2028.

U.S.-Taiwan relations will remain strong but shaped by election politics. The U.S.-Taiwan ART is a key risk point. If Section 301 findings spur debate over market access, agriculture and labeling, the opposition may delay ART review, increasing the risk of U.S. trade pressure and friction.

Taiwan’s trade surplus with the United States continues to widen, driven by AI-related demand and Taiwan Semiconductor Manufacturing Company (TSMC). The economy grew 14.6 percent in the first quarter of 2026 with a projected 9.6 percent annual growth rate, which would represent the country’s strongest economic expansion in 16 years. Exports to the United States in 2025 rose 78 percent year on year (or up US$86.9 billion) to US$198.3 billion. A similar surge in 2026 would heighten political sensitivity despite ART.

Defense spending remains contested. On May 8, 2026, Taiwan’s opposition-dominated Legislative Yuan passed a US$24.8 billion special defense budget (TWD 780 billion), cutting the Executive Yuan’s original US$40 billion proposal (TWD 1.3 trillion) by about US$15 billion (38-40 percent) and narrowing it largely to U.S. arms procurement while excluding many domestic defense and industrial programs. Failure to advance spending toward 5 percent of GDP could create bilateral headwinds with the Trump administration later in 2026.

Macroeconomic Climate

The AI-Driven Economic Surge: Balancing Hyper-Growth with Inflationary Pressures

Taiwan’s economic landscape for the latter half of 2026 is defined by an extraordinary “AI Shield,” with the Directorate General of Budget, Accounting and Statistics aggressively revising its GDP growth forecast upward to 9.6 percent. This surge is powered by a dual-engine recovery in exports and private investment, as global demand for advanced semiconductors and AI infrastructure reaches historic highs. Unlike the dot-com bubble of 2000, current growth is anchored by tangible demand in advanced packaging and high-end server procurement, with key players like TSMC reporting high revenue visibility and limited overbooking risks. Taiwan’s stock exchange is now ranked fifth globally on the back of TSMC’s success and the ecosystem in which it is centered.

However, the economy exhibits a notable “industrial divide.” While the digital and semiconductor sectors are thriving, traditional manufacturing industries face headwinds from rising energy costs and cooling end-user demand in non-AI segments. Domestic resilience is further bolstered by a buoyant stock market and government policies — including minimum wage hikes and tax optimizations — which have sustained private consumption despite inflationary concerns.

To maintain long-term stability, the government continues to monitor the unemployment rate — currently hovering near historic lows — and export orders, which serve as the primary pulse for Taiwan’s export-dependent economy. While the Central Bank remains vigilant, government energy subsidies have successfully kept the consumer price index at a manageable 1.9 percent, shielding the public from the full impact of global commodity volatility. BGA offers three scenarios in light of the current global economic uncertainty:

Upside Scenario: Accelerated global AI integration leads to record-breaking export orders and sustained capital investment. In this scenario, deescalating geopolitical tensions over Iran lower energy costs, allowing GDP to surpass 8 percent as traditional sectors recover alongside the tech boom.

Moderate Scenario: AI remains the dominant growth driver, with GDP hitting the forecast 7.1 percent. Domestic consumption grows at a steady 2.6 percent, supported by stock market wealth effects and wage growth, while inflation remains controlled under the 2 percent threshold.

Downside Scenario: Prolonged Middle East instability — exceeding 150 days — triggers “stagflationary” pressures. Rising imported fuel costs squeeze margins for non-AI industries and dampen consumer purchasing power, leading to a wider economic gap and more cautious U.S. corporate spending.

Investment Environment

Strategic Capital Influx: Research and Development Localization and Frontier Resilience

As Taiwan solidifies its role as the global nerve center for AI infrastructure, the investment environment is shifting from “pure manufacturing” toward a high-value research and development and data hub. Beyond semiconductor expansion, Taiwan is witnessing a surge in foreign direct investment driven by Taiwan-U.S.-Europe “non-red supply chain” collaborations, ensuring secure and resilient technology ecosystems. This strategic influx is now centering on robotics and unmanned aerial vehicle supply chains, leveraging Taiwan’s precision engineering to meet global security and automation demands.

However, the rapid scaling of these advanced sites places pressure on local infrastructure. To maintain appeal, the government is streamlining land acquisition for strategic industrial zones and prioritizing smart grid integration. For multinational firms, the focus has shifted toward utility stability and “green premiums,” ensuring that localized research and development for AI and autonomous systems meet corporate and government sustainability mandates. Nevertheless, Taiwan is likely to continue to struggle to produce enough renewable power to meet the demands of industry.

We will continue to keep you updated on developments in Taiwan as they occur. If you have any comments or questions, please contact BGA Senior Adviser Rupert Hammond-Chambers at rupertjhc@bowergroupasia.com.

Best regards,

BGA Taiwan Team