Energy, Climate and Resources Forecast

WHAT YOU NEED TO KNOW

- The impact of the landmark U.S. Inflation Reduction Act, signed into law in August 2022, continues to reverberate across the region, driving policy responses from advanced economies under pressure from domestic economic interests to compete on fiscal incentives.

- Japan was first out of the gate to promulgate a national-level response through the Green Transformation Act.

- Australian Prime Minister Anthony Albanese outlined his Future Made in Australia vision, operationalizing his country’s ambitions to become a green energy superpower and spur domestic industrial investment.

- It has been a tumultuous period for Asian gas markets amid restructuring and recovery from the Russia-Ukraine war. Uncertainty is growing in response to supply-side interventions from major liquefied natural gas (LNG) suppliers like the United States and Australia, most recently with the Biden administration’s LNG export permitting pause.

ON THE HORIZON

- Expect more national legislative frameworks and industrial policies using “carrots” to drive emission reductions in pursuit of national targets and avoid missing out on the energy transition’s economic dividends.

- BGA expects increasing policy convergence between climate action and global trade. China’s dominance of existing clean energy technology supply chains, fixation on carbon leakage and protectionist inclinations to bolster the efficacy of growing industrial policy frameworks will require targeted trade policies and complementary trade regimes.

- Pressure is mounting on Asia’s high emitters to adjust course and demonstrate credible pathways to meet 2030 emission-reduction targets. Multilateral forums will become increasingly strained as members diverge in climate progress. Following the alignment of Asian chairmanships of global multilateral forums last year, Asian economies will be less able to determine the agendas and discourse on greater flexibility in climate commitments.

- Expect continued emphasis on biofuels development and deployment as emission-reduction pressures converge with existing energy security and trade balance motives. ASEAN is pushing stable biofuel feedstock supply with supportive agriculture-related policies and incentives. For example, Indonesia and Malaysia increased mandates for biodiesel blending and have cut exports to stimulate domestic consumption.

Sector Overview and Forecast

Macrotrend Monitor

Urgency To Address Climate Change Reshapes Regional Policies and Investment Strategies

The Indo-Pacific is witnessing significant shifts in its energy landscape, with focus on low-carbon transitions driven by rapid economic growth and escalating environmental concerns. A key element of this transition is the integration of renewable energy sources, which are seeing substantial growth across many countries in the region. China, India, Vietnam and Japan are leading the way in solar and wind energy investments, while Southeast Asian countries, including Indonesia, are exploring geothermal potential and biomass energy solutions to diversify their energy away from traditional fossil fuels.

The urgency to address climate change is reshaping regional policies and investment strategies. The commitment to achieve net-zero emissions has gained momentum, catalyzing developments in advanced technologies such as carbon capture, utilization and storage (CCUS), battery storage solutions, mining and minerals processing, hydrogen energy and biofuels. The push toward electric vehicles and the establishment of green infrastructure have heightened trends that are receiving significant governmental and private sector investment. These initiatives are not only aimed at reducing carbon footprints but are also seen as crucial to secure energy resilience and sustainability in a region prone to energy import dependency and environmental challenges.

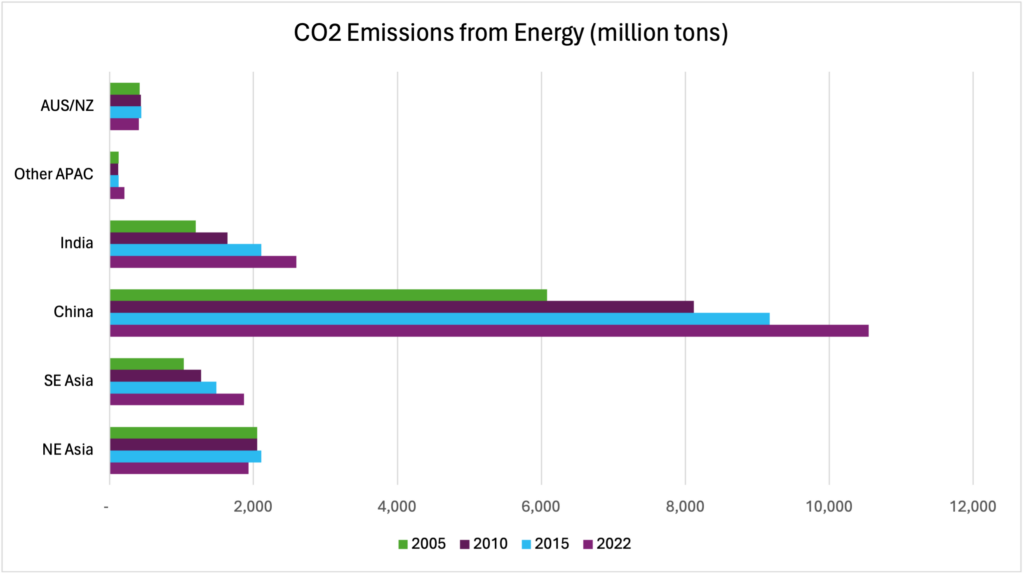

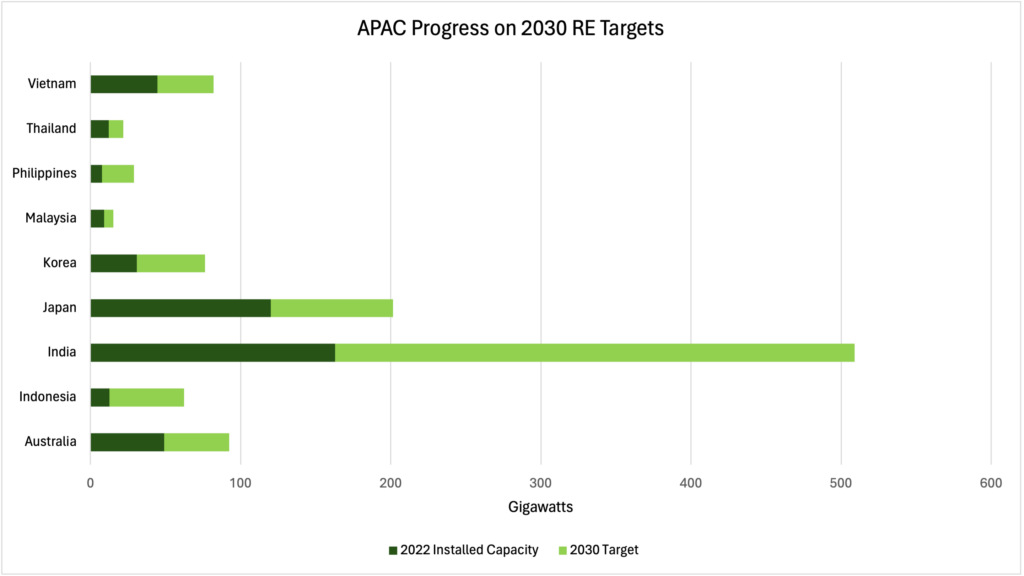

Despite all the positive developments in the Indo-Pacific’s move toward a lower-carbon economy, the region has also experienced challenges in progressing along a pathway to achieve national determined contributions for emission reductions. In addition to higher interest rates that disproportionately affect capital expenditure-intensive renewables projects, disagreements about climate financing, entrenched power sector stakeholders and other nonfinancial barriers are impeding progress toward 2030 goals as expressed in renewable capacity deployment and emissions growth (see figures).

These unique regional dynamics serve as a counterweight to the impressive cost declines in renewable technologies. The challenges highlight the complexities of aligning diverse stakeholders with varying economic interests and environmental goals.

Subsector Highlight

Carbon Capture and Storage Makes Progress in Key Sequestration Jurisdictions

In the face of these headwinds, Indo-Pacific economies are evaluating a wide range of climate solutions and demonstrating policy sincerity and momentum in new technological pursuits. In particular, carbon capture and storage (CCS) policies have seen significant advancements, especially regarding their integration into Indonesia’s and Malaysia’s unique energy frameworks in 2023. These countries are pioneering regional engagement and the implementation of CCS initiatives, which are crucial in balancing rapid industrial growth with environmental sustainability.

Indonesia set the stage for CCS policy advancement in the region with its recent enactment of Presidential Regulation No. 14, exemplifying the country’s commitment to attract international investment in CCS capabilities and infrastructure. This regulation is designed to fortify the legal and operational framework surrounding CCS and CCUS projects. It marks a pivotal development in incorporating these technologies into Indonesia’s wider energy and environmental strategies.

However, the implementation of this regulation is tedious and involves multiple government bodies, including the Ministry of Energy and Minerals, the Ministry of Investment and the Coordinating Ministry of Maritime and Investment. Political disagreements and the differing priorities among these ministries have stymied progress on implementing guidelines, including efforts to modify existing regulations to include CCS/CCUS in the existing cost recovery scheme.

In the coming months, BGA expects Indonesia’s Ministry of Energy and Mineral Resources to introduce a ministerial regulation to address the technical aspects of CCS operation, such as exploration, permitting procedures and safety standards. Concurrently, the government will update business procedures to better define the CCS licensing process as distinct from traditional oil and gas regulatory requirements.

For companies operating in hard-to-abate sectors like steel, cement and chemicals, these developments open a much-needed decarbonization pathway by better aligning policy frameworks with growing corporate ambitions for net zero.

In the latter half of this year, Malaysia’s energy sector is expected to begin to roll out its National Energy Transition Roadmap. Although the road map sets an ambitious goal of turning Malaysia into a CCS hub for Southeast Asia by 2025, the vision is aspirational given the challenges in regulatory and legal framework developments needed to support such advancements. Petronas is at the forefront of exploring CCS development through various partnerships and research initiatives, yet substantial groundwork is required to realize these objectives fully.

The political dynamics in Malaysia, particularly in the states of Sabah and Sarawak in Borneo, continue to shape the energy policy landscape. The appointment of Deputy Prime Minister Fadillah Yusof, who also manages Sabah and Sarawak affairs, to oversee the energy transition portfolio underscores the strategic significance of these states. This restructuring could either harmonize or complicate interactions within the federal government, depending on how state and federal agendas align.

Sarawak is making strides in its carbon trading policies, setting legislative benchmarks for carbon markets that may encourage similar actions across the nation. However, these developments should be viewed as preliminary steps toward enhancing Malaysia’s standing in the global carbon market. As Malaysia approaches these initiatives, it is crucial to manage expectations and recognize the aspirational nature of these goals within the broader regional context of Southeast Asia’s energy transition.

We will continue to keep you updated on developments in the energy, climate and resources (ECR) sector as they occur. If you have comments or questions, please contact BGA Senior Director Bradford Simmons at bsimmons@bowergroupasia.com.

Best regards, BGA ECR Team