Thailand Forecast: Political Stability Amid Growth Constraints and Investment Challenges

WHAT YOU NEED TO KNOW

- Thailand’s political stability has strengthened under the Bhumjaithai Party-led coalition, which holds a clear parliamentary majority. This stability reduces near‑term political risk while raising expectations for policy effectiveness, particularly on economic performance, cost‑of‑living pressures and investor confidence.

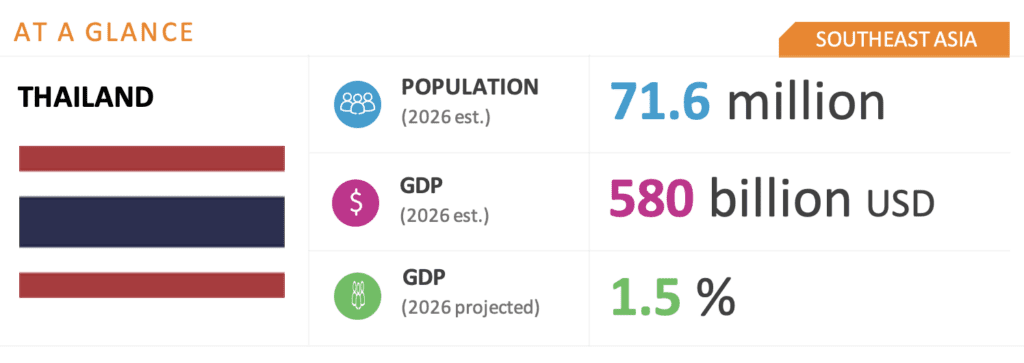

- The baseline GDP growth forecast hovers around 1.5 percent for 2026, lagging other Southeast Asian economies. Downside risks are intensifying, contingent on the duration of the Iran war and potential escalation across the wider Middle East, which could heighten energy price volatility and push growth below 1 percent.

- The investment outlook remains cautious amid weak domestic demand, fiscal constraint and high household debt. Policy‑supported sectors such as electric vehicles (EVs) and electronics continue to attract selective private investment while public investment underpins limited economic activity. The new government plans to raise investment to around 30 percent of GDP in the next three to four years, focusing on fiscal consolidation, streamlined approvals and structural reforms.

ON THE HORIZON

- Key political dynamics for the second half of 2026 will be the government’s ability to deliver urgent policy directions and initiatives against the backdrop of heightened geopolitical uncertainty, rising energy prices and slower growth. While a technocrat‑anchored Cabinet has been appointed, policy formulation and execution will continue to operate within the constraints of a stable yet transactional coalition government.

- The Iran conflict will continue to place pressure on the government’s cost‑relief and safety-net measures, fuel subsidies and monetary policy accommodation. Fiscal flexibility, including an upward public debt ceiling adjustment, is expected to provide additional room to cushion economic activity if growth conditions deteriorate.

- Progress on permit‑streamlining measures, direct power purchase agreements and key public-private partnership infrastructure projects will be critical to sustaining investment momentum. Prolonged energy‑market volatility could continue to limit a broader private‑investment rebound.

- Thailand’s hosting of the International Monetary Fund-World Bank Annual Meetings in October will provide avenues to reinforce policy credibility, showcase reform priorities and reengage global investors.

Thailand Market Overview and Forecast

Political Climate

New Government Heralds Political Stability and Policy Continuity

Thailand enters the second half of 2026 with a stable political environment following the formation of Anutin Charnvirakul’s Bhumjaithai Party-led coalition government, which holds an overwhelming parliamentary majority and is positioned to administer over a full four-year term. Current stability reflects a functional alignment between the governing coalition and the conservative establishment, lowering the likelihood of political disturbances. Nevertheless, several factors warrant monitoring, including controversial Cabinet appointments that could attract constitutional scrutiny, ongoing corruption‑related cases and potential coalition friction between the Bhumjaithai and Pheu Thai parties. While unlikely to destabilize the government, these dynamics could complicate governance and policy coordination.

With post-election coalition government formation largely settled, attention has shifted to the government’s policy deliverables. The government faces mounting challenges from weak growth, rising energy prices and geopolitical spillovers, which place pressure on both policy execution and public confidence. At issue is the government’s capacity to demonstrate credible progress and satisfy expectations. Weak delivery could increase opposition scrutiny in Parliament and public dissatisfaction, especially among urban and younger voters.

Following its election loss, Thailand’s opposition is weakened but still relevant as the People’s Party continues to exert influence through urban support and parliamentary scrutiny. The government and legislature are expected to continue advancing constitutional reform following voter referendum approval to replace the military-led 2017 charter. Movement on constitutional reform would likely attract scrutiny from conservative stakeholders, but stalled progress could draw criticism from reform‑oriented constituencies, making the referendum process a key indicator of the government’s political standing.

Macroeconomic Climate

Fragile Growth Outlook Amid Structural Constraints and External Geopolitical Pressures

Thailand’s economic outlook for the latter half of 2026 remains fragile, with weak recovery dynamics amplifying exposure to global uncertainties. Despite post-election stability, escalating Middle East tensions and Thailand’s reliance on imported energy have pushed up costs and constrained growth. Key sectors are under pressure as high fuel and raw material costs weigh on industrial sentiment and tourism faces declining long-haul demand and fewer high-spending Middle Eastern tourists. Export-oriented industries are affected by supply disruptions, weaker Gulf demand and the uncertainties surrounding U.S. tariffs following Section 301 investigations. In response, the government has rolled out targeted relief measures, such as a co-payment handout scheme and diesel subsidies. Meanwhile, the central bank maintains an accommodative policy rate of 1 percent.

Upside Scenario: If the Iran conflict is resolved in the first half of 2026, Thailand’s annual GDP growth is projected at 1.4 percent, with inflation at 2.8 percent. While energy prices ease, they remain above pre-conflict levels. The impact is largely contained, though recovery is gradual.

Moderate Scenario: If the conflict persists into the second half of the year, growth is expected to slow to 0.8 percent and inflation to rise to 4.6 percent. Prolonged energy pressures and supply chain disruptions would raise production costs, squeeze margins and weaken household income, increasing the risk of stagflation.

Downside Scenario: If the conflict persists throughout 2026 and spills into 2027, GDP growth could fall to 0.7 percent, with inflation rising to 4.9 percent. The shock would become increasingly structural, as sustained cost pressures erode purchasing power and sharply slow business activity. Contracting global demand and ongoing supply disruptions would weigh on exports and tourism, while policy constraints would limit the pace of recovery, heightening the risk of prolonged stagnation.

Investment Environment

Investment Momentum Moderates as Selective Inflows and Partnerships Anchor Growth

Thailand’s 2026 investment outlook remains cautiously resilient, supported by the selective realization of foreign direct investment commitments in high‑value and policy‑aligned sectors, such as data centers, EVs, semiconductors and renewable energy infrastructure. Total investment is projected to expand 1.8 percent in 2026, decelerating from 4.9 percent in 2025 as investment momentum remains subdued amid soft domestic demand and high household debt. The Board of Investment’s record investment applications in 2025 are expected to translate into actual capital expenditure in the second half of 2026.

Public investment is expected to grow 1.7 percent in 2026, down from 8.9 percent in 2025, reflecting tighter fiscal conditions amid mounting global headwinds. Despite the near‑term moderation, large‑scale infrastructure projects are expected to gain traction, supported by a THB 1.4 trillion ($43 billion) transport budget allocated to 20 projects under public-private-partnership arrangements. Key projects include double‑track railways, airport expansions, new expressways, the land-bridge project connecting the Gulf of Thailand and the Andaman Sea and renewed focus on the Eastern and Southern Economic Corridors.

The new government’s investment promotion measures focus on addressing administrative bottlenecks rather than introducing new incentive schemes. The “Thailand Fast Pass” has been introduced to expedite investment application approval while the “Super License” aims to consolidate multiple approvals into a one-stop process. The government aims to streamline regulations to promote investment by strengthening Board of Investment incentives, advancing the Draft Clean Air Act to align with energy requirements for global companies and enabling direct power purchase agreements to improve access to renewable energy. The new government targets an increase in investment to 30 percent of GDP from 22 percent within the next three to four years, driven primarily by higher public and PPP‑led infrastructure spending and selective private investment flow. The impact is expected to materialize over the medium term rather than an immediate acceleration in headline growth.

We will continue to keep you updated on developments in Thailand as they occur. If you have any comments or questions, please contact BGA Thailand Managing Director Teerasak “Art” Siripant at tsiripant@bowergroupasia.com.

Best regards,

BGA Thailand Team