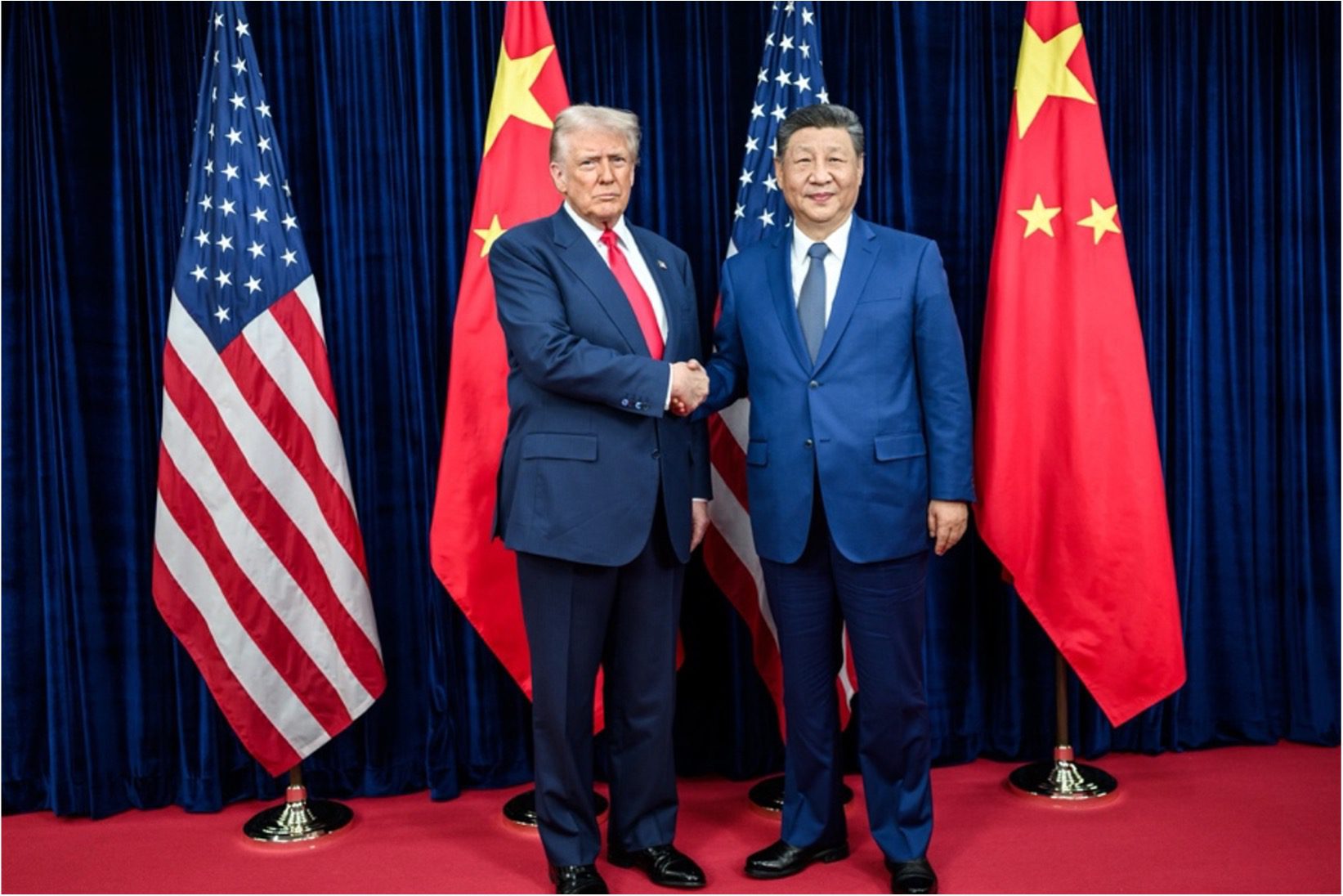

Trump and Xi Meeting Yields Updated US-China Framework Deal

BGA China Adviser Eric Wang and Account Manager Sam Overholt wrote an update to clients on China’s fourth plenum.

Context

- The meeting between Presidents Donald Trump and Xi Jinping in Korea October 30 signals a reversible ceasefire built around quarterly tariff rollovers, a pause on new U.S. export controls, a Chinese deferral of rare-earth export curbs and staged Chinese purchases of U.S. agriculture products. These “deliverables” are wrapped in face-saving optics such as leaders’ visits, a pathway to resolving the TikTok impasse and a reprieve on port fees on each other’s ships. The framework is headline-heavy but verification-light. China’s commodity purchase offer — especially of soybeans — suggests Beijing is preserving its options rather than locking in fixed U.S. volumes. Notably, the fentanyl-linked tariffs have been reduced by 50 percent, with cooperation on precursors now proceeding through law-enforcement channels rather than tariff instruments.

- The Trump administration is touting the outcome as a breakthrough and has even labeled the summit as a “G2”meeting on social media, referring to a time during the great financial crisis when U.S.-China cooperation was crucial to stabilize the global economy. This seems to suggest Beijing is framing the current leaders’ consensus as a template for global economic stability in the Trump era. While some focus shifts from tariffs to verification — through data-sharing pilots, enforcement benchmarks and independent audits — the broader punitive U.S. tariff structure remains in place. Overall, Washington and Beijing have sketched a pause that lowers near-term friction without rewriting the rulebook.

- Beijing is unlikely to agree to sign a detailed purchase or enforcement agreement. A formal instrument would narrow its room to maneuver if prices, supplies or domestic priorities shift. That puts more weight on process over paper in Washington. If the Supreme Court trims presidential tariff authority in the coming months, the administration will likely lean on the new Section 301 investigation into China’s implementation of the “phase one” agreement of 2020 as a statutory backstop. Evidence, real or perceived, of China not living up to its commitments could prompt the United States to recalibrate its reciprocal tariffs.

Significance

- On export controls, the United States is freezing planned expansions — most notably shelving for one year the Commerce Department’s “affiliates rule,” which would have automatically extended restrictions to majority-owned subsidiaries — while signaling no new Section 232 moves. Beijing, for its part, is deferring its rare-earth export controls for roughly a year pending review.

- In parallel, United States Trade Representative Jamieson Greer said the United States will postpone for a year its Section 301 investigation into China’s maritime, logistics and shipbuilding sectors — including delaying prospective fees on Chinese commercial vessels calling at U.S. ports. China’s Ministry of Commerce confirmed it will suspend its retaliatory port fees as well. The net effect is a measurable reduction in immediate supply-chain and maritime risk, but not a structural rollback of the broader tit-for-tat regime.

- On purchases, Beijing is broadcasting its intentions to make “substantial” agriculture buys — soybeans being foremost — sequenced over the next two to three quarters. There is no binding purchase commitment, but the signal is giving China the flexibility to lift U.S. cargoes during calendar windows when Brazilian supplies are tight or overpriced.

- Through official channels, China has only said the United States and China reached a joint arrangement in Malaysia to address each side’s trade concerns. The statement ties this to the recent leaders’ meeting in Korea, where the two presidents agreed to strengthen economic and trade cooperation. Beijing says it is ready to work with Washington to uphold and implement the leaders’ consensus.

- While these arrangements lower the immediate temperature and operational risk and preserve leverage on both sides, the durability of the agreements will hinge on whether the promised year of restraint yields verifiable progress rather than a simple reset of the escalation clock. Expect new flashpoints to shift into adjacent areas of technology and economic rivalry: EV supply chains and batteries, artificial intelligence chips and tooling, industrial software, data governance and cybersecurity reviews. The United States will carefully monitor China’s possible circumvention of tariffs and rules by shipping through third countries. Friction will also show up in compliance and enforcement of today’s “consensus in principle,” including rare earth element exports, licensing transparency, fentanyl-precursor enforcement and verifiable agriculture flows.

Implications

- The political calendar is doing extra work, with a Trump visit to Beijing likely in April, and potential high-level meetings on the sidelines of the Group of 20 summit in Florida next year are possible as well. These meetings are momentum-maintenance events that steady markets and stakeholders while technical issues are hashed out.

- Separately, the United States has opened an additional Section 301 investigation into implementation of the 2020 “phase one” agreement. That review functions as a statutory backstop to preserve the ability to adjust reciprocal tariffs if the U.S. Supreme Court narrows presidential authority in this area.

- On Beijing’s side, maneuvering room remains. Recent upgrades to its trade arrangements with the Association of Southeast Asian Nations and China’s resilient trade performance give Beijing options as it calibrates purchases, enforcement steps and timing. The detente can hold in the near term, but only if both sides keep re-earning it with concrete actions. Its half-life will be tested by enforcement drift, third-country routing and pressure to re-weaponize industrial policy tools. Companies should plan for a managed freeze with periodic stress events, not a stable equilibrium.

We will continue to keep you updated on developments in China as they occur. If you have any comments or questions, please contact BGA Adviser Eric Wang at ewang@bowergroupasia.com or Account Manager Sam Overholt at soverholt@bowergroupasia.com.

Best regards,

BGA China Team

×